Shifting into Low Gear Reduced economic momentum suggests cyclical slowdown is taking place although recession will be avoided To avoid cracks widening in the economy, Europe will look towards fiscal stimulus to support domestic demand growth

by Samuel Duah

Our central scenario is one in which growth moderates but does not result in recession. Nonetheless, serious cracks are forming in Europe’s economy that highlight the potential for lack of reform to generate a more serious slowdown if the world economy weakens further.

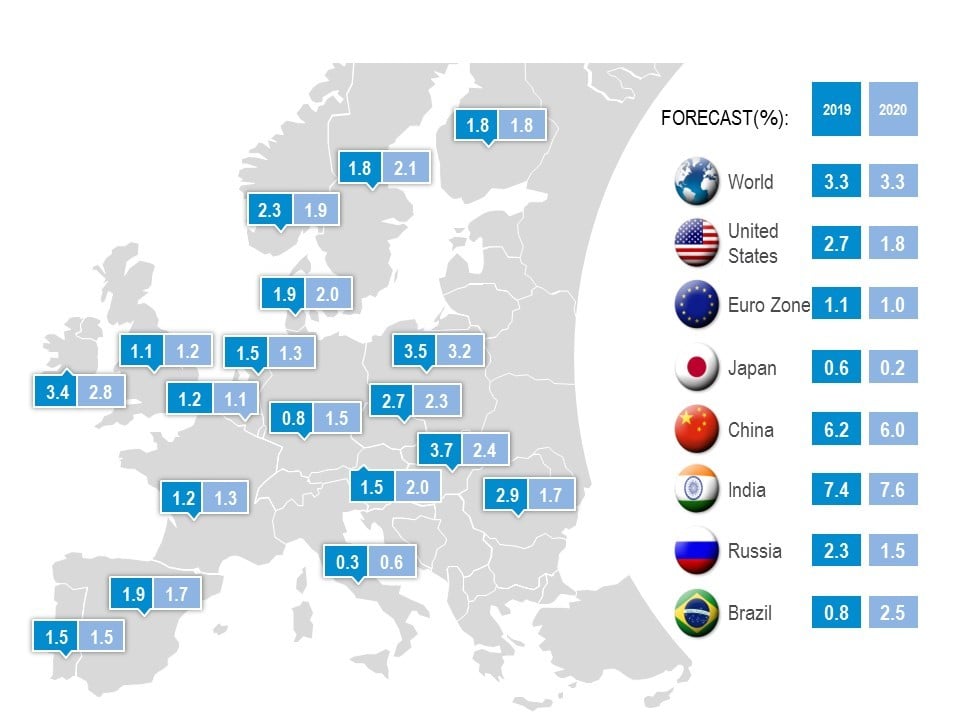

Growth picked up in Q1 2019, following the sharp deceleration at the end of 2018, with Eurozone GDP at 0.4% (1.2% pa) and EU28 at 0.5% (1.5%). BNP expects slow momentum in growth for 2019. The Eurozone is forecast to come in at 1.1% and the UK at 1.3% for 2019 (assuming Brexit damage is contained). With a cooler economy, inflation expectations are moderating, with Eurozone inflation projected at 1.3% and the UK at 1.9%, both lower than in 2018.

Expansion of protectionism seems to be contained for the moment. Brinkmanship has ceded to a (albeit volatile) negotiation process between the US and China which may result in a new bilateral deal. The ripples from brinkmanship continue to wash over the global economy from trade induced reduction in economic activity.

The slowdown in Europe is primarily manufacturing-led, with Germany among the worst affected with industry hit by declining export orders, although the country saw expansion (0.4%) again in Q1 2019. Elsewhere, Italy entered recession in 2018 and left in Q1 2019 while, in contrast, Spain maintained good growth (0.7% in Q1) and France is stable at 0.3%. The UK continues to see growth, even with Brexit uncertainty, indicative of the greater contribution of services to growth.

The two main risks to external growth stem out of uncertain outcomes from China’s stimulus program to stabilise the economy and from the US with fading effects of the Trump tax cut.

Consequently, Europe cannot rely on exporting its way to growth. Europe will have to look far more to its own domestic market over the next two years with the two support mechanisms: monetary and fiscal policy.

Monetary policy is reaching the end of its effectiveness with central banks signalling the end of unconventional measures. It is also a time of transition for the European Central Bank (ECB) and Bank of England (BoE), where both governors are due to step down.

Cooling in the economy spooked the ECB enough in March 2019 to reactivate LTRO lending to banks to avert credit drying up and triggering a self-generated downturn. Unlike the BoE, the ECB will probably slow the pace of its normalisation policy.

Europe will look more towards fiscal policy to support domestic demand. Unlike monetary policy there is no fiscal union, with policy coordinated mainly by the Stability and Growth Pact; limits to meet euro obligations.

Assuming these limits are not challenged, the ability to spend depends on the health of individual government finances. Over time, wider differentials in economic performance may emerge in European economies to impact the relative performance of real estate's occupational base.

Source: BNP Paribas Real Estate. European Commission