Late Cycle A slowing economy has potential to create weaker outcomes on real estate's occupational side Investment performance though will prove durable across the upcoming year

By Samuel Duah

Transaction volumes reached €264bn in 2018 and are solid at the start of 2019. Real estate investment is likely to see out 2019 in better shape than the occupational market

Economic slowdown worries are tilting investors back to bonds, where yields are under downward pressure. This is to real estate’s benefit and favours steady conditions over the forecast period.

2019 is seeing real estate performance metrics move into the single-digit phase of the cycle. Given the state of the asset universe, the relative performance of real estate looks positive. The best results continue to be driven by property with superior income return

Real estate investment is likely to see out 2019 in better shape than the occupational market. Investment transaction volumes reached €264 billion in 2018, only 1% below 2017. Q1 2019 investment totals (€43 bn) are lower (down by 21% over Q1 2018 ) although still above the 10 year average.

To understand real estate’s strength is to appreciate the nature of the Late Cycle, the point at which economic expansion ceases and the defensive qualities of assets come to the fore.

The expenditure definition of economic growth is a composite measure - a sum of consumption, investment, government spending and net exports. It is the net exports side of this equation that is not powering properly: a direct result of the chilling effect that trade disputes are having on the global economy. The slowdown is being led mainly by the manufacturing sector but felt less in services which is the majority user base of real estate.

In addition, inflation is decreasing and employment increasing in Europe as the service sector generates jobs. Both are good proxies that indicate there is large spare capacity in the economies of Europe.

From this perspective it is possible to argue that Europe never attained the peak associated with the expansion phase, and slowdown is a result of being caught in the backwash from US growth entering its late cycle stage.

What slowdown does mean, the UK aside (and even here there is large Brexit induced doubt), is that the timeframe for normalizing monetary policy in Europe is elongated.

We continue to hold the view that 2019 will witness the end of central bank policies of liquidity injections with the cessation of central bank support. As a result, nominal bond yields may remain flat over most of 2019 before rising.

Tepid economic growth with lower likelihood of bond increase will continue to keep real estate returns in most markets in single digits and close to zero in some cases.

As before, it is the prime segment with its historically low yields where returns will be most sensitive to relative changes in asset pricing. This is particularly acute with Europe’s volatile political situation, which may manifest itself into a flight to quality if populism (with its demand for a new settlement) grows stronger.

The twin engines of good occupational performance and stable capital markets are humming into 2019. Durability of occupier markets in the face of overt economic slowdown is remarkable but understandable when weakness is in one specific area of the economy. Even so, it is unrealistic to expect this situation of both real estate engines running perfectly to persist across the year. There are more uncertainties surrounding prospects for the occupational side of the real estate market.

The occupational engine is likely to start sputtering first. Trade dispute induced slowdown is a marginal impact on primary real estate users in the services sector. Nonetheless many occupiers have already undertaken major relocation moves and others may end up being hesitant about real estate commitments while the economic outlook is hazy. BNP expects the economic slowdown to persist over 2019 and this is likely to translate into a more generalised slowdown in the occupational market. That is likely to manifest in marginal vacancy rate increases and slowing rental growth.

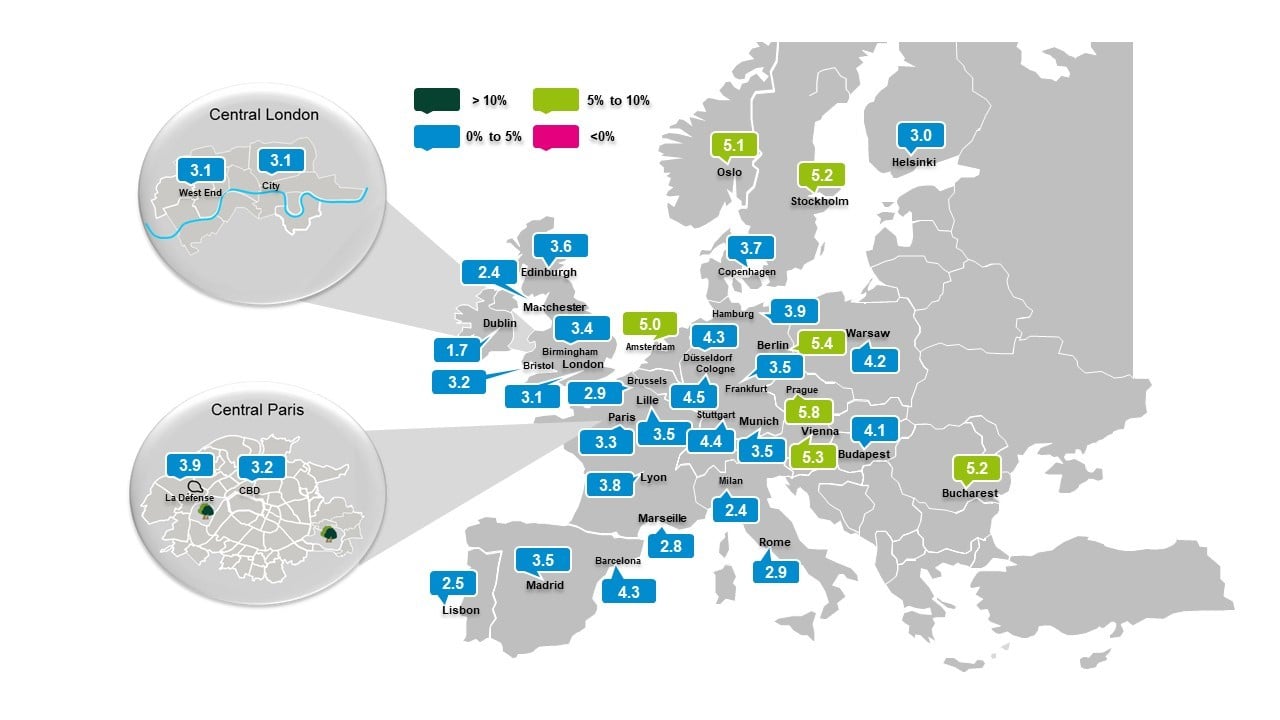

We expect prime rental growth to be low for offices ranging between -1.20% to +5.0% over the forecast period. Markets at the lower end include Budapest (-1.2%), Marseille (-1.0%), Dublin (-0.6%) and Manchester (-0.8%), while those at the upper end include Oslo (+5.4%), Berlin (+4.1%), Amsterdam (+2.8%) and Cologne (+2.7%).

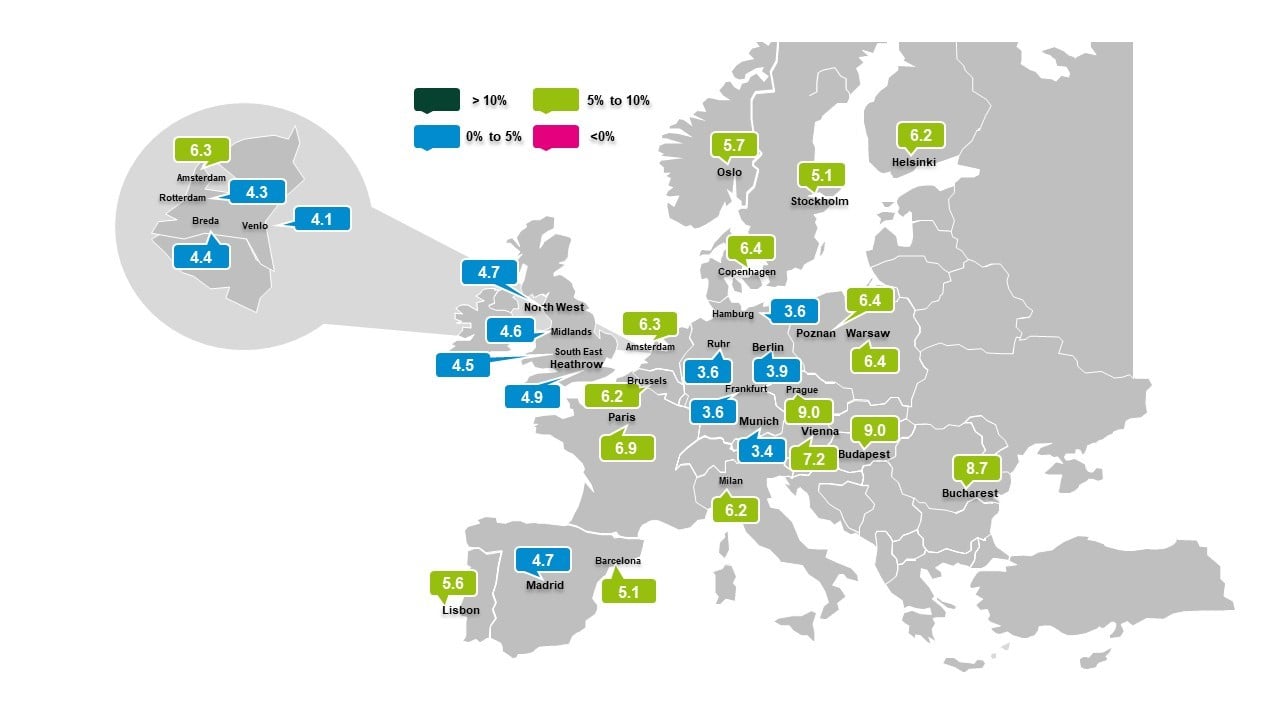

Logistics prime rents are projected to show a narrow but mostly positive range between 0% and 3% across Europe over the forecast period as the market catches up with other real estate sectors. Warsaw is the only market forecast to experience no growth in rents, while fellow CEE market, Prague, shows the strongest rental performance at 2.9%.

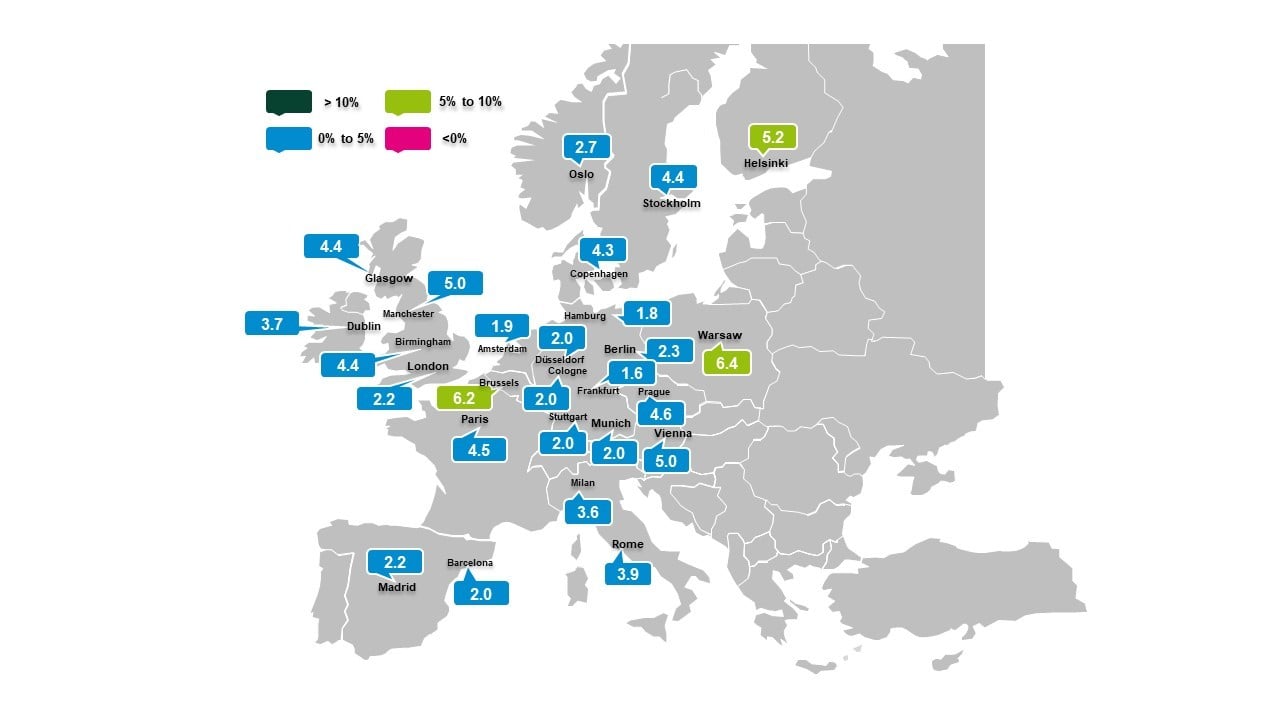

Prime rents in European retail also present a narrow range, with greater propensity to negative outcomes than logistics. At the bottom, we see rents declining in all the German cities plus Central London over the forecast period. The strongest rental growth will be seen in Milan (3.1%), Dublin (3.3%) and Paris (3.5%) over the five-year forecast period. Given these locations are city centre prime, this represents the upper end of what can be expected in this sector, which remains under severe pressure across Europe from e-commerce penetration.

Economic uncertainty presents renewed pressure on bonds due to their perceived safe-haven status. As a result, European real estate yields will remain mostly stable across 2019. In offices there is still some scope for compression, as seen in Paris and Lyon, and the CEE cities of Vienna and Prague. All UK offices are already seeing decompression and by 2020, all European office yields will be either stable or expanding.

Logistics yields have a slightly longer stay of execution on decompression with most remaining stable in 2019 and some still falling; the strongest compression is occurring in France and in CEE markets.

Retail is a more mixed picture with compression still ongoing in Vienna while Berlin, Munich and Prague will move from compression in 2019 directly into increases in 2020 These are outliers, as most European retail markets are poised for increases in yields having ceased compression.

We still hold the view that rental increases will not fully mitigate yield decompression on capital values. Consequently, all sectors and the majority of markets will see capital value decline in 2019 and 2020. For offices, we think there is still some growth left in French markets and CEE markets. Over the forecast period, office capital growth will be most robust in Berlin, Oslo and Vienna; all above 2% pa. Logistics will see strongest capital growth in Vienna (1.8% pa), Greater Paris (2.6% pa) and Prague (3.5% pa).

With such low capital growth, returns will inevitably be in the single-digit territory and come from income. Overall total return from the office market is expected to average 5.5% pa over the five-year forecast period and driven more by income (+5.2%) than capital growth (+0.6%), reflecting the late stage in the investment cycle.

It will be enough for the investment market to see out 2019 in better shape than the occupational market. For offices we expect prime returns will go from 1.7% (Dublin) to 6.5% (Oslo).

Logistics will exhibit the greatest spectrum in prime return, ranging from 3.4% (Munich) to 9.0% (Prague), with retail the narrowest range at 1.7% (Frankfurt) to 5.2% (Helsinki).

Returns remain front-loaded in the forecast, reflecting the fall-off in capital values over the later part of the period.

Source: BNP Paribas Real Estate (% average p.a.)

Three potential triggers

Global Economy: The world economy is looking at a particularly binary outcome at present. Resolution of the China-US trade dispute will result in positive upside to the global economy, which will do much to restore the confidence of real estate occupiers. Conversely, it could go the other way and erode confidence further, leading to downturn

Bond Yields: Bond yields are back under pressure. For real estate that could see yield stability prolonged further if it persists..

Real Estate Development: Vacancy rates have fallen to lows but if speculative supply delivery accelerates beyond the capability of the occupational market to absorb, a situation of oversupply may occur.