Running to Stand Still European economies are converging again albeit at lower levels Creating an effective policy mix is the greatest challenge in 2020 for European governance

In late 2019 the global economy experienced a stabilisation. The important factor here was the improvement we saw in manufacturing, which was largely down to the relative calm in trade disputes. The impact of protectionism seems to be somewhat underestimated, as the scale is large enough to affect future global economic growth. Despite this, the prospects for global growth are much lower with both the Chinese stimulus and US fiscal boost eventually fading

It is against this backdrop that European economies, many that have growth largely dependent on global trade, are operating. We do not expect a recession in Europe. Instead, countries face the prospect of years of persistently low growth.

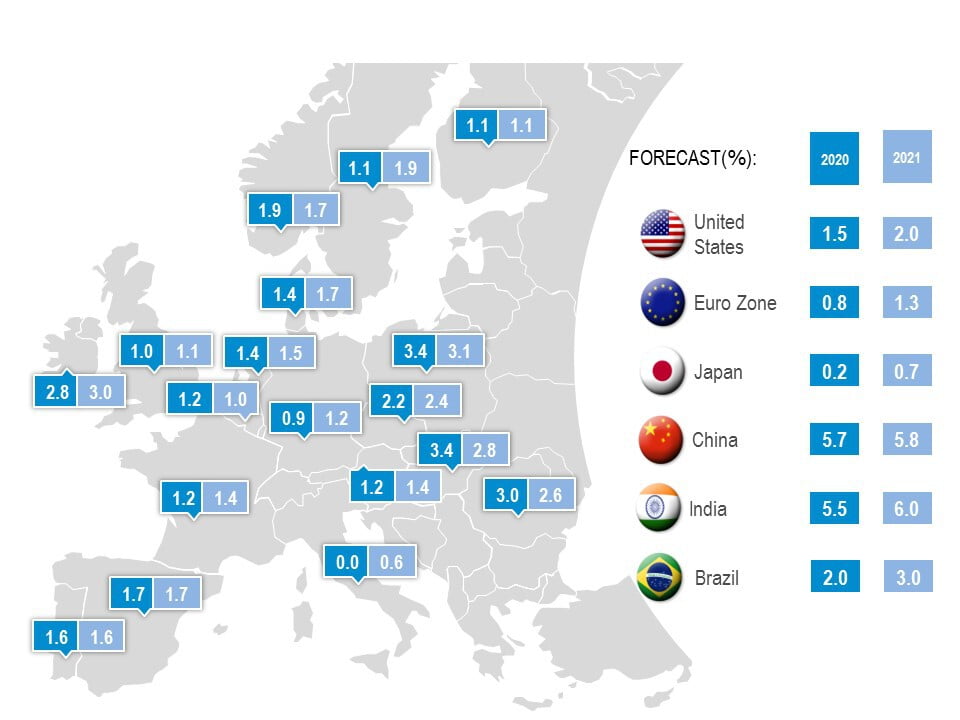

In aggregate, the economic growth rates of European nations are likely to converge again albeit at lower levels. This is mainly a result of slowing Central and Eastern European economies as the impact from stalled foreign direct investment takes its toll. Eurozone GDP is likely to reduce from 1.1% in 2019 to 0.8% in 2020 and 1.3% in 2021 (BNP Paribas). Of the big 5 European economies, Italy struggles the most with growth of 0.2% in 2020 and 0.7% in 2021, followed by Germany (0.4% in 2020 and 1.2% 2021). Spain is the strongest (1.7% 2020 and 1.3% 2021). France is 1.1% in 2020 1.3% in 2021. The UK, now officially outside the EU, may see expansion of 1.1% in 2020 and 1.7% in 2021, due to the boost provided by increased government spending.

Europe may experience weakness associated with a recession but unlikely to experience any steep rises in unemployment. The labour markets remains a bright feature and sustained expansion here is indicative of the strength of the service sector that accounts for over 60% of employment.

BNP Paribas forecast an unemployment rate of 7.7% for the Eurozone and 3.8% for the UK in 2020. Unemployment below its pre-crisis level, together with low inflation, means real wage growth is occurring, supporting domestic demand.

Subdued inflation means that there is little pressure to move interest rates upwards. With resumption of asset purchases in 2019, monetary policy will remain supportive for longer. Growth concerns are encouraging safety seeking behaviour and long-term interest rates are back in negative territory in core countries such as Germany.

Monetary policy is effectively at a standstill or run its course, which has prompted the ECB to conduct a review on how to re-ignite growth.

Which is why we will see a greater focus on fiscal policy. European nations are considering introducing growth-enhancing fiscal measures in 2020 to support the domestic sector. Pre-crisis levels of growth seem unattainable partly due to governments accumulating debt since then. The more debt-laden countries of Europe may struggle to ensure their make policy mix is as effective as intended. As a result, differentials in growth may emerge across Europe.

Source: BNP Paribas Real Estate. Consensus Forecasts

Sukhdeep Dhillon