Closing the Gap An economy running to standstill will encourage investors to seek assets with the best balance of safety and return Real estate investment will be a clear beneficiary of this behaviour

Transaction volumes reached € 281 bn in 2019 with a number of markets attaining new highs. Transaction volumes will be lower in 2020 as supply issues become more prominent

Unspectacular economic growth is the backdrop for real estate. It is creating sufficient worry to encourage safety-seeking behaviour with bonds and incentive to invest in real estate for the income difference

2020-2024 will see real estate performance metrics converge across Europe, particularly for yields. Performance is positive across all segments although the best results come from property where investors can improve income return

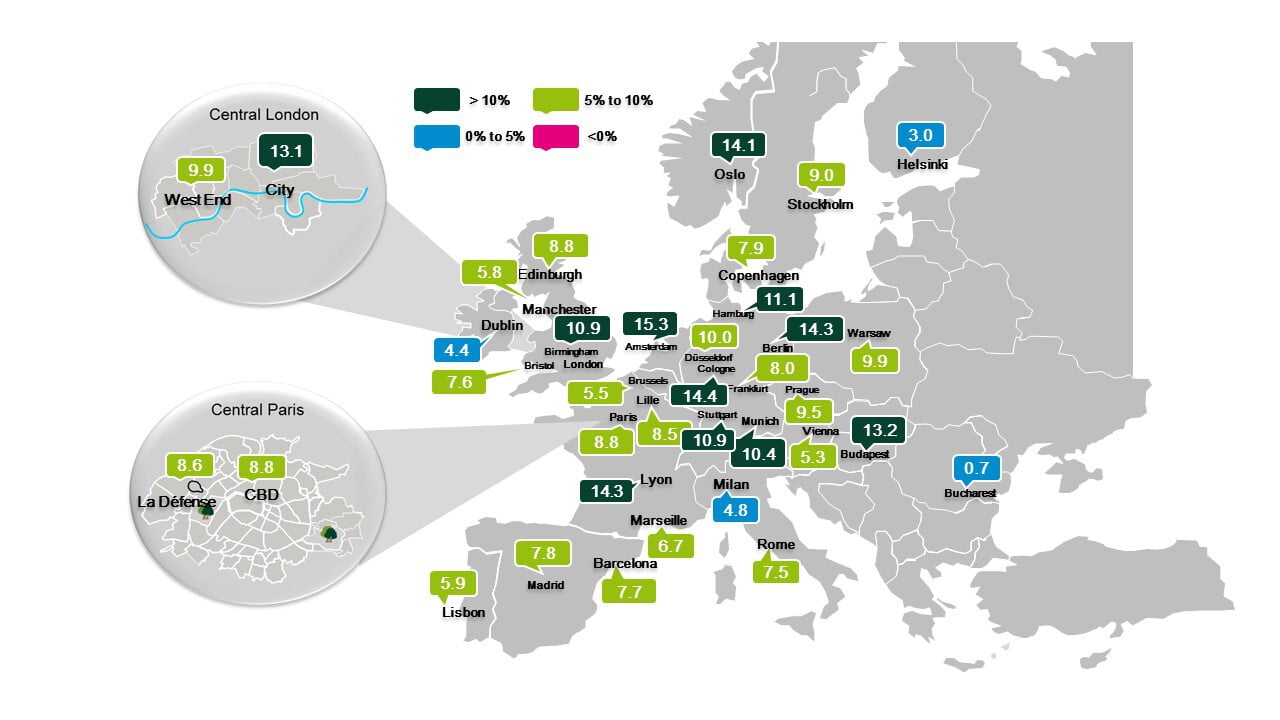

European investment volumes reached €281 billion in 2019, an increase of 2.6% over 2018. A number of country markets across Europe posted new highs in transactions. Top here is Germany at €73 billion followed by France at €41 billion. Sweden (€13 billion), Italy (€12 billion) and Spain (€10 billion) also recorded new historic highs.

It is an extraordinary situation given how late in the cycle real estate is. More so given the expensive pricing attached to investing in core assets in major European cities. Prime yields in all these markets are at historic lows led by Germany (2.6%) and France (2.8%).

The worries created by the trade-induced slowdown prompted increased enthusiasm for sovereign debt as a means to preserve capital. Investment focused on developed nations where the supply is limited and pushed government bond yields in core European markets deeper into negative territory. There remains a very large pool of investors who share bondholders’ desire for safety, but still want the profit that comes with investing.

Safety seeking behaviour is encouraging this type of investor to ignore expensive pricing, and increase their allocations to core real estate in key western European city markets. The attractions are relative liquidity with the assurance that there will be a buyer at disposal plus the strongest occupational markets to generate income from capital allocation.

Economic growth is likely to stay low across the forecast period with near zero interest rates and inflation running below central bank target rates. The attraction of real estate in this environment implies even greater competition for core property, thereby sustaining transactional activity, albeit at lower levels.

By restarting the quantitative easing program in 2019, the ECB is signalling less effort to normalise monetary policy over the near future. The Bank of England is an exception as it has more room to cut interest rates but it may only restart asset purchases if the situation warrants with the Brexit trade agreement. What this means is the chance of meaningful increases in bond yields is now so low that it is far more likely to see real estate yields move downwards again.

The dynamic created by safety seeking behaviour is unlikely to abate if yields in real estate continue to compress and, more importantly, align over the forecast period. Depending on the type of investor, their strategic goals and time-frame, buyers of lower quality real estate assets may find this situation unsettling. The alignment of yields elevates the relative risk of mispricing.

In a more fuzzy investment environment, intimate understanding of the source of income matters: income generation will be the defining market performance measure over the forecast period.

The service sector is the main employer of people and principle driver of office occupation. Consequently, trade dispute induced slowdown continues to represent a marginal impact on real estate primary users. There is sufficient labour market momentum to support expansion in office occupation and, in turn, rental growth over the front part of the forecast period at least. Critical to prolonging expansion of employment will be the confidence of companies in making business investments. It may be that the market has yet to experience the full consequences of changes here in hiring intentions.

Yet low economic growth will eventually take its toll on occupational performance in an indirect way through changes in occupational patterns. Across Europe, medium sized deals (beloww 5000 sq m) drove office occupation in 2019 in contrast to larger transactions that characterised the previous two years. Occupiers in the recovery phase of the economy undertook major relocation moves to take advantage of new space at an acceptable cost. The European market of 2019 and going forward is characterised by the lack of modern Grade A space with large floorplates – a universal feature across European cities. That necessitates pre-lets in developments for occupiers with large floorplate requirements, especially in CBDs. Without pre-lets, financing for developments is difficult and the uncertainty created by low economic growth will only inhibit development further.

This structural factor is likely to translate to a slower occupational market. Along with the development pipeline, it will manifest in marginal vacancy rate increases in the office sector. The region with the lowest vacancy, Germany, is likely to see vacancy increase from 3.1% in 2020 to 4.1% in 2021. What we are talking about here for most regions is a move from 'very low vacancy' to 'low vacancy' by the end of the forecast period.

We expect prime rental growth for offices in cities to range between -2.0% pa to +5.0% pa over the forecast period. Gateway cities are likely to see growth slow from 3.8% in 2020 to 1.8% by 2024. Regionally, Benelux may see the sharpest fall back from 5.6 in 2020 to 0.8% by 2024. Germany may scale back from 6% in 2020 to 1.9% in 2024 and Southern Europe from 2% to 0.8% in 2024. Regions that may see little change include France, which will move from 2.2% to 1.9% in 2024; Nordics from 3.2% to 2.8% and CEE from 0.6% to 0.5% with a dip into negative mid forecast. The only region likely to see stronger growth at the end of the forecast is UK and Ireland moving from 2.5% to 2.9% in 2024.

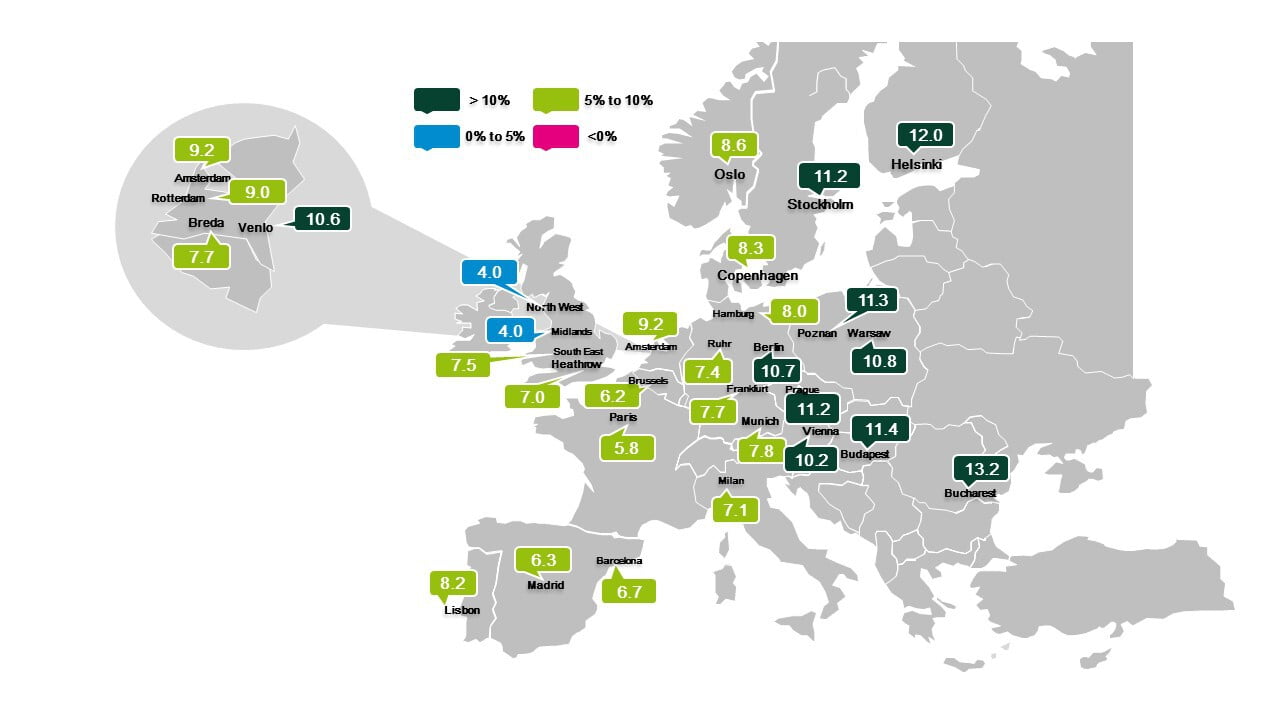

The logistics market differs from offices as supply and demand are highly aligned in the sense that occupiers frequently build their own supply. Critically low supply in many markets results in a high amount of design and build, so land acquisition is the determining factor. Consequently, logistics prime rents may show a positive range between 0% and 5% across Europe. Regionally the momentum of rental growth is likely to fall back towards the end of the forecast. The sharpest example of this are the Nordics that drop from 8% in 2020 to 0.8% in 2024. France will remain unchanged at 1.8% with other regions halving from around 2% in 2020 to below 1% in 2024.

Unlike offices and logistics, an excess of retail property still exists as e-commerce continues to impact the sector. It is unlikely that we will see the bottom of rental decline while a structural surplus exists. Prime rents in European retail continue to present a narrow range, with propensity to negative outcomes. Gateway cities, which present the best of European retail, may see rental growth of 0.7% in 2020 increase slightly mid forecast before returning to 0.7% by 2024. The region showing strongest rental growth both across and at the end of the forecast is CEE with 3% in 2020 and 1.5% in 2024 reflecting the development of modern retail outlets.

The outcome of continued transaction activity is the narrowing of yield gaps. What we are likely to see in Europe is the convergence of prime yields in the core CBDs and with equivalent prime property in regional cities. Arbitrage may see the gap between prime and secondary property of the same asset class narrow sharply. At pan European level, we may also see narrowing between sectors, although this will not completely close given the different dynamics. The downside will be a degree of fuzziness in pricing.

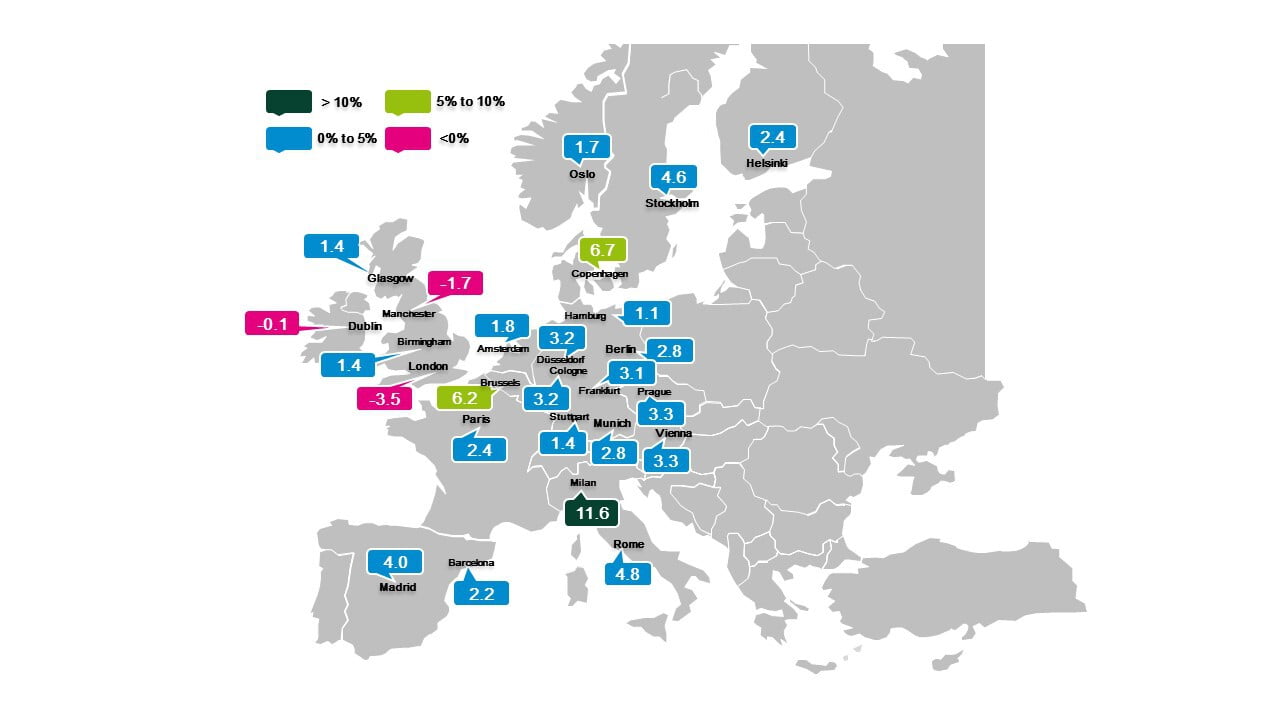

The United Kingdom, London offices especially, stands out in a scenario of more compression. Brexit worries resulted in cocooning of yields for three years following the referendum vote. Yields have been static compared to the rest of Europe creating the unusual situation of City of London offices on par with Prague at 4%. With exit from the EU now a reality and stronger government, transactional activity is sure to generate compression. The UK (and Nordics) will be the only region to see positive office capital growth across the whole of 2020-2024.

The economic backdrop suggests that offices may experience a further two years of compression before rising towards the forecast end 2023/24. Regionally France may be lowest at 2.65%. Germany as whole is at 2.68% though Berlin may go down to 2.50%. By 2022, the UK may reach 3.43% (London West End will be 3.35%), Nordics 3.44%, Southern Europe 3.51% and Benelux 3.49%. CEE may bottom put earlier in 2021 at 4.29%

Compression in the logistics yields also has longer to play out. Decompression is likely manifest midway through the forecast for all regions except the CEE, which may continue to fall in 2023. The strongest compression regionally in 2020 and lowest yields may occur in Germany with a fall to 3.6%, followed by Nordics and CEE markets. Logistics will see capital growth at the front of the forecast period before it falls away in most regions from 2023 onwards. Retail will mostly be in decompression from 2020 onward with the exception of Southern Europe and Benelux where yield expand from 2021 onwards. Gateway cities may see yields increase from 3.13% to 3.16% in 2020 rising to 3.30% by 2024. Capital growth in retail will remain mostly negative over the forecast period.

Investors need to accept that returns from real estate will stay low for the near future. 2020 is likely to see the last year of double-digit return in the office market at 10.2 % for all European prime offices. It may fall to 3.0% by 2024. Europe office market returns in 2020 may be 9.2% and fade to 3.6% by 2024. Logistics total return may be 9.3% in 2020 for Europe, falling to 4.3% in 2024. European retail at 2.4% in 2020 may see a small increase in prime total returns to 3.7% by 2023

Returns stay front-loaded in the forecast. Although yield compression is occurring, capital growth will be extremely low so income will inevitably dominate in returns. Real estate is entering an income-driven universe.

Source: BNP Paribas Real Estate (% p.a.)

From Macro to Micro

Systemic risk reduced: Greater clarity exists in the direction of the world economy. Barring unexpected events, the economy is looking at a protracted period of low growth with few shocks, but few boosts either. This alters the emphasis from macro to micro risks for the forecast

Sector Risks: Issues specific to real estate sectors will take precedent. The specific risk is reduction to income quantum. For offices, stalling employment growth in the service sector; for logistics it is the lack of supply for occupiers; for retail, the magnitude of e-commerce penetration may be greater on shops in the city core

Country Risks: Reordering of the European system following Brexit may change forecast outcomes. Here we look at the UK, where tougher outcome on Brexit trade negotiations may reduce the yield compression built into the forecast

Samuel Duah