Arable crops: AHDB & FW. Prices are ex farm. Future prices are indicative bids from agricultural traders. Livestock: FW. Beef R4L steers and lamb R3L specification. Future prices from outlook reports. Milk: DEFRA.

World market supply and demand is driving domestic markets, with weather and production concerns in western Europe, northern America, south America and the Baltics, on various crops, all having impacts on domestic markets. Demand remains strong, stocks remain tight, creating the likelihood of large market moves depending on good or bad news being produced. UK prices are showing signs of cooling slightly in early September following news of a large Australian wheat crop and harvest pressure. Overall prices appear to be relatively well supported for the time being.

Harvest yields have been extremely variable this year even within regions. Late frosts through April, a very wet May and lack of sunshine through to harvest meant that some crops were very poor this year. However that is not the case for all and plenty of growers have seen yields at or above their long term average. Quality has also been variable, with rain at harvest once again causing problems for later-cut milling wheat.

The recently increased wheat price of roughly £30/Tonne when combined with an average yield of 9.5 Tonnes per hectare, equates to more than the whole BPS rate. It should be noted therefore that although some farmers' profit margins will look healthier this year, they should not forget about the volatility of the commodity markets, and should not put off decision making about the loss of BPS in the coming years.

Winter barley yields have generally been lower than average due to adverse spring conditions when the crop wished to push on. That said indications of high straw yields will be a considered bonus. Spring malting barley yields have been close to average and quality has been reasonable in most areas.

OSR - likely to have a renaissance with much better crops in field than past years. Flea beetle damage last autumn was significantly lower than previous year, adverse wet winter conditions will have hampered some root structure, but yields have generally been as expected for many growers.

Beans - There are some excellent looking crops in places, good growth and pod fill conditions. However, evidence of fusarium foot rot in many fields highlighting soil compaction and health issues will have hampered some crops to the point of destruction, so there is likely to be varied results.

Sugar Beet - low indications of virus yellows compared to 2020, which caused up to 50% yield losses, and recent rains will help crop development.

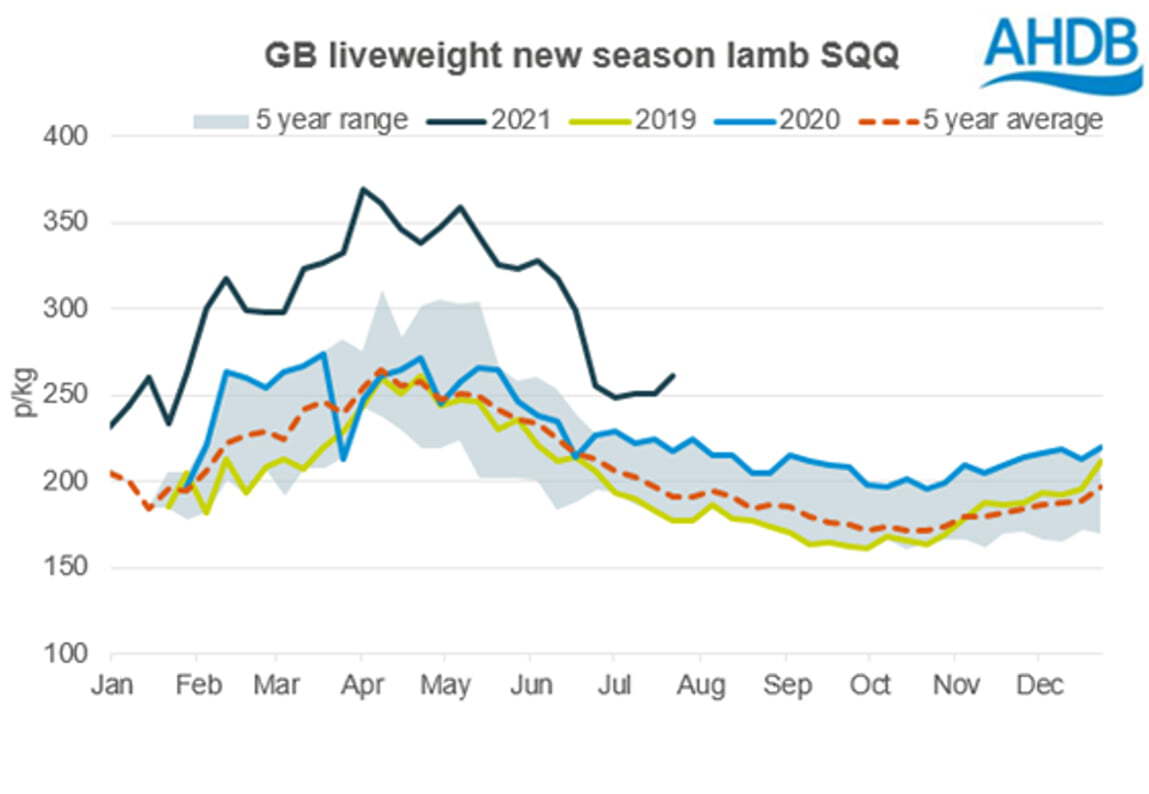

Lamb prices remain supported and are well above their 5-year average too at 548p/kg deadweight (Farmers weekly) after a peak in the spring of 648p/kg deadweight. The support for lamb prices appears to be driven by low slaughterings in the UK this year, it appears shepherds are holding onto more ewe lambs to re-build flocks after the pre-Brexit rush to reduce flock size.

Source: AHDB, LAA, IAAS

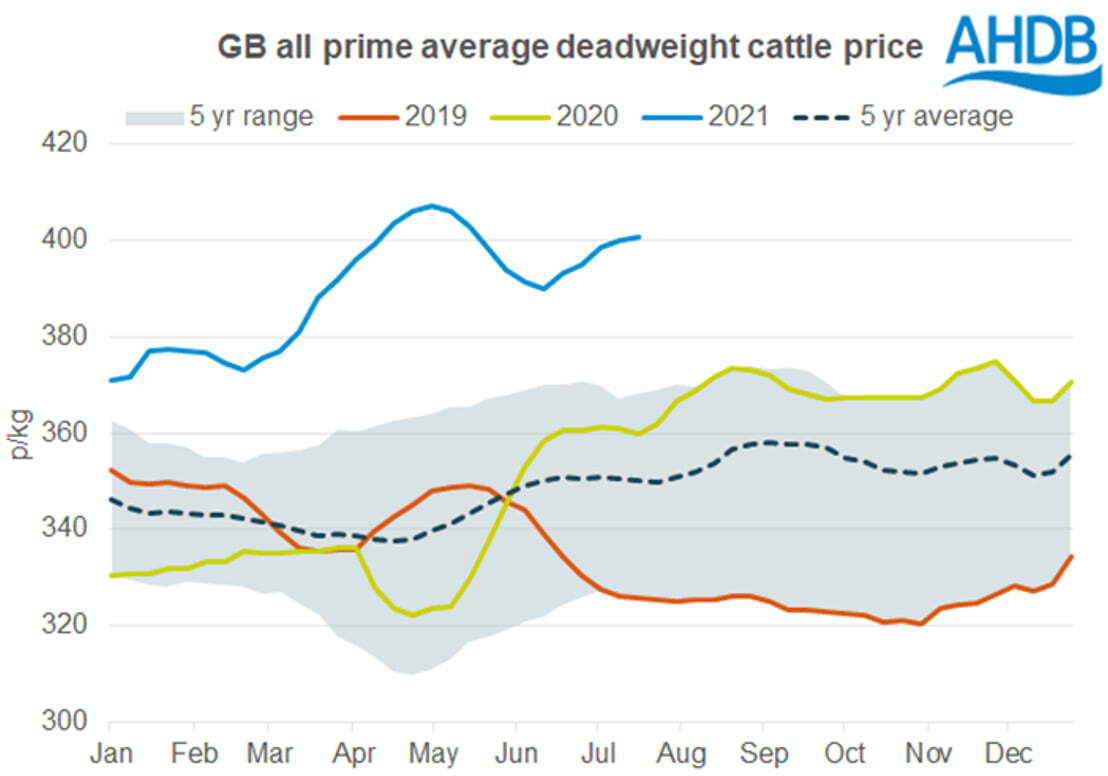

UK prime cattle deadweight average price is well above the 5-year average at 409/kg in late August (AHDB). These high prices appear to be supported by a long term decline in the numbers of beef cattle in the UK, while the global supply is being absorbed by growing demand for beef worldwide. In the short to medium term prices look to continue to be well supported and AHDB reports of increased demand for beef from supermarkets in recent weeks.

Source: AHDB

UK Production of Milk hit an early peak this spring and has dropped a long way since there. Dry conditions in mid-July is likely to hit production further before the autumn block calving cows come back online. The UK average milk price for May 2021 was up to approx. 30.02ppl (AHDB).

News that China’s pig herd is recovering after the swine flu epidemic will put long term pressure on the pork market. In the short term pig prices have recovered since the winter up to 158p/kg deadweight this July (AHDB).

Source: https://ahdb.org.uk/pork/gb-deadweight-pig-prices-uk-spec

DECC data reports red diesel has continued to rise in line with wider fuel prices to 67.3ppl for August 2021, while diesel at the pump was at an average of 137ppl.