Office investment activity in the South East for Q4 2020 stood at £857m, down only 1% on Q4 2019. Q4 2020 was significantly up (+163%) on the previous quarter albeit it was the third lowest quarter on record, but nevertheless a good indicator of returning investor appetite. Although this represents a slower year for South East office investment, total volumes reached £2.35bn across 81 transactions, down just 7% on 2019.

The sale of White City Place, W12 was the largest transaction to complete in Q4 where Cadillac Fairview purchased the property from Mitsui Fudosan for £235m. Other notable transactions included Brunswick’s purchase of Carlson Court, 116 Putney Road, SW15 for £23m, which attracted significant interest.

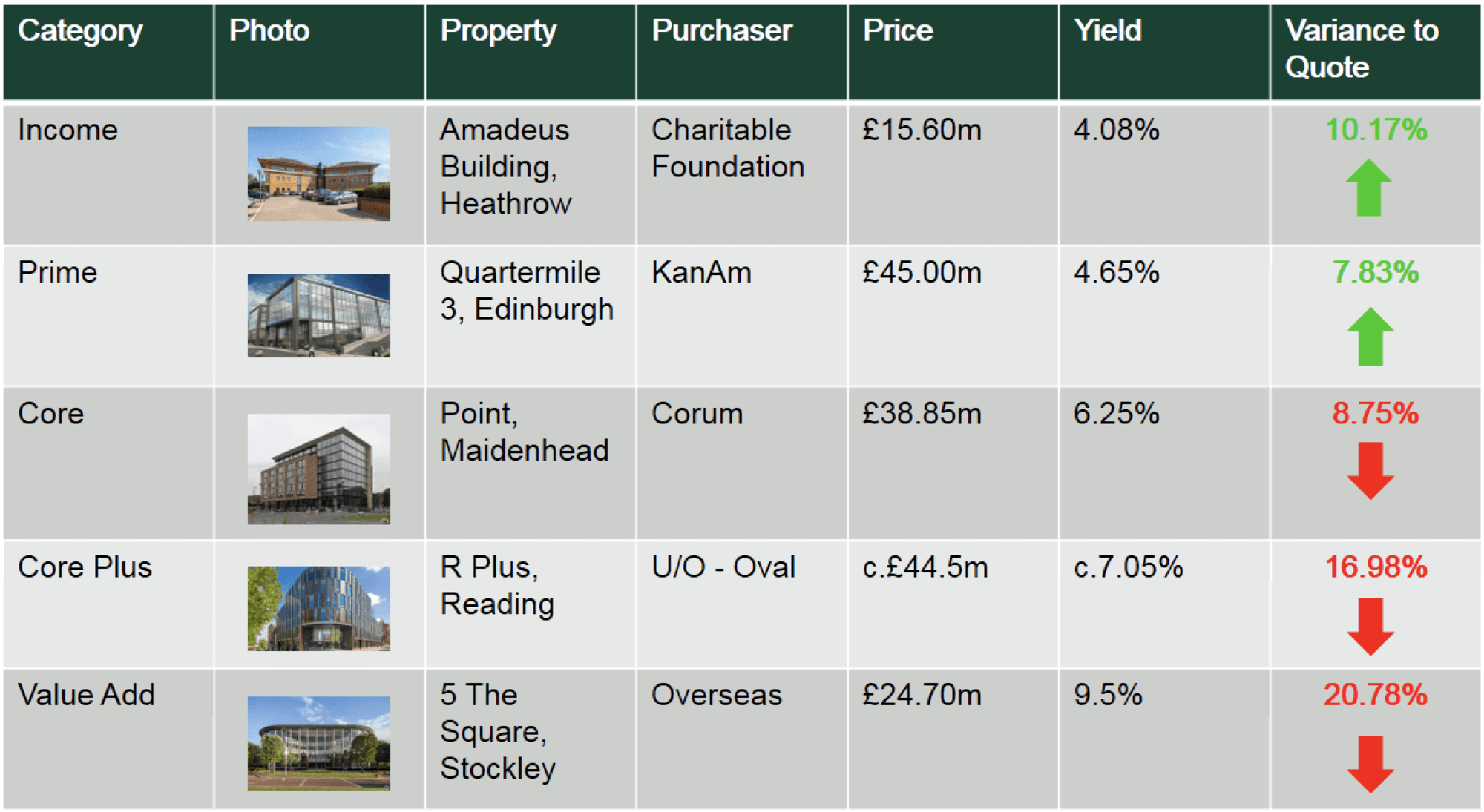

There is no shortage of investor capital with demand from European institutions and Overseas for prime and income while significant funds have been raised by private equity for core plus and value add assets. Overseas investors dominated volumes in Q4 taking a 42% share.

Looking ahead, Q1 2021 has started positively with realistic vendor pricing and a continuation of Q4’s volumes is expected to follow through based on assets under offer. The office market is witnessing a K shaped recovery whereby: ultra prime and well let (10 years +) pricing hardening while core, core plus and value add pricing is drifting by varying degrees.

Whilst the occupational return to offices will be on a gradual basis dependant on the easing of restrictions, tenants will place greater importance on high quality physical environments in order to attract staff into the workplace rather than expect them to attend.

K Shaped Recovery

See next page for current National Office price movement